🇺🇸 Wall St #WeekAhead Alphabet, Intel results in focus for AI trade as US earnings rev up - Reuters https://t.co/lAzo6pLCGL #WallStreet #AI #Earnings #US

🇺🇸 Wall St #WeekAhead Alphabet, Intel results in focus for AI trade as US earnings rev up - Reuters https://t.co/lAzo6pLCGL #WallStreet #AI #Earnings #US

🇺🇸 #SPX | Are “Magnificent 7” Companies Still Top Contributors to S&P 500 Earnings Growth for Q2? -Factset https://t.co/LFrORawRFE https://t.co/0IYrmjQvuq #SPX #Magnificent7 #EarningsGrowth

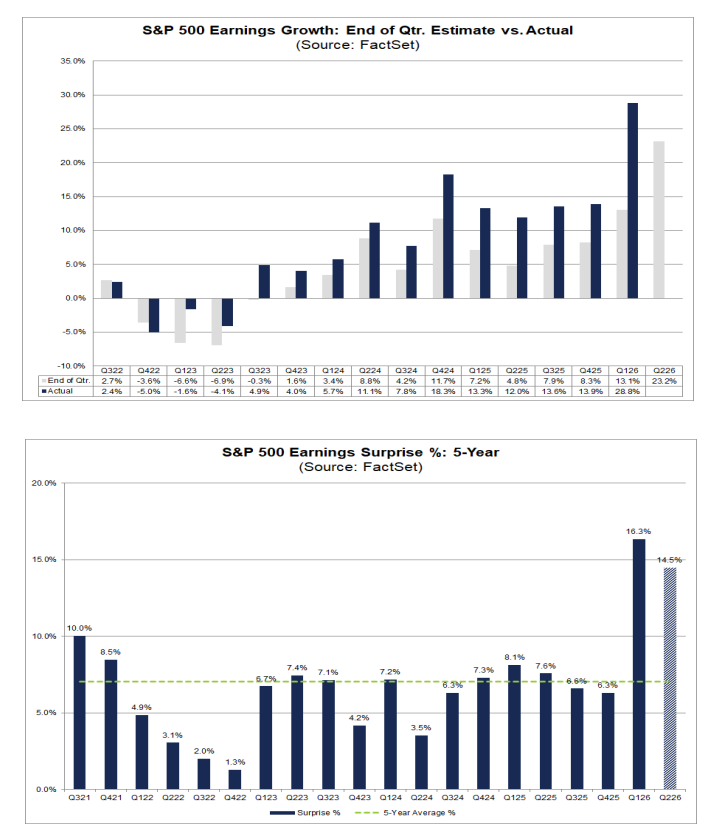

🇺🇸 #SPX | S&P 500 Likely To Report Earnings Growth Above 29% for Q2 - Factset https://t.co/QNxQhxpKt7 https://t.co/ab3vuLS5Sa #SPX #EarningsGrowth #Factset #US

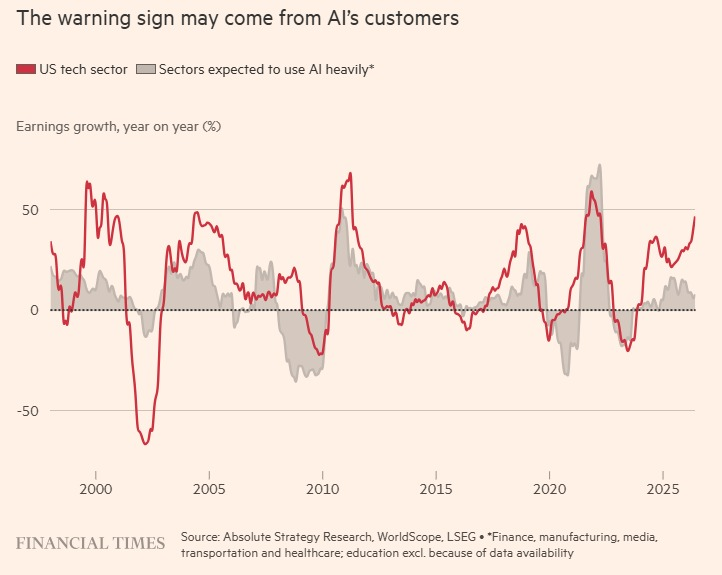

🚨 The real warning signal for AI may not come from the tech giants but from their customers. ➡️ For now, the infrastructure sellers continue to capture most of the value but the sectors expected to use AI heavily are not yet showing a spectacular acceleration in earnings. https://t.co/wnFq7bH729 #AI #TechTrends #CustomerInsights #Thetweetdoesnotmentionanyspecificcountries.Therefore #therearenocountrycodestoreturn.

People are most unhappy when their own earnings are considered to be unfairly low and when the rich seem to earn too much. Unfair low earnings of the poor and being unfairly advantaged oneself are not part of the equation. Empirical studies suggest that inequality #IncomeInequality #UnfairEarnings #SocialJustice #Nospecificcountrycodescanbeidentifiedinthegiventweet.

🇨🇳 #China A-Share Profit Preview Flags Signs of Robust Growth - Securities Daily ➡ China’s A-share companies are beginning to release first-half earnings guidance, with early disclosures pointing to robust growth in select sectors, Securities Daily reports, citing analysts. #China #AShares #EarningsGrowth #CN

🇺🇸 *MICRON SEES 4Q ADJ. REV. $49B TO $51B, EST. $43.24B - BBG *MICRON 3Q ADJ. REV. $41.46B, EST. $35.69B *MICRON SEES 4Q ADJ GROSS MARGIN ABOUT 86%, EST. 83.6% *MICRON 3Q ADJ EPS $25.11, EST. $20.49 *MICRON SAYS CUSTOMERS’ RAPIDLY GROWING DEMAND #Micron #EarningsReport #TechIndustry #US

UFFICIALE UEFA: INTER ESCE DAL SETTLEMENT La Prima Camera dell’Organo di Controllo Finanziario dei Club UEFA, il CFCB, ha completato la valutazione dei club sottoposti a settlement agreement, chiamati a rispettare specifici obiettivi legati ai risultati economici calcistici nella stagione 2025/26. Nella sua valutazione, la Prima Camera del CFCB ha tenuto conto del significativo e inatteso crollo dei ricavi da diritti televisivi nazionali che ha colpito i club francesi nella stagione 2025/26 e che continuerà ad avere effetti anche nella stagione 2026/27. L’Olympique Marsiglia non ha rispettato l’obiettivo finale previsto dal settlement agreement, non essendo riuscito a conformarsi alla football earnings rule nella stagione 2025/26, relativa ai periodi di rendicontazione chiusi nel 2023, 2024 e 2025. Considerando la portata limitata della violazione e il già citato crollo dei ricavi televisivi nazionali, la Prima Camera del CFCB ha imposto al club le seguenti misure disciplinari: esclusione dalla prossima competizione UEFA per club alla quale il Marsiglia dovesse qualificarsi nelle prossime tre stagioni, a meno che il club non rispetti l’obiettivo economico previsto per la stagione 2026/27; limitazione alla possibilità di registrare nuovi giocatori nella Lista A per le competizioni UEFA della stagione 2026/27; multa da 6 milioni di euro. La Prima Camera del CFCB ha inoltre accertato che l’Olympique Marsiglia ha violato anche la regola sul costo della rosa, avendo registrato un rapporto superiore al 70% per l’anno solare 2025. Tenendo conto dell’entità dello sforamento, al club è stata inflitta un’ulteriore multa da 4 milioni di euro. Per quanto riguarda i club ancora sottoposti a settlement agreement, la Roma ha superato leggermente l’obiettivo intermedio fissato per l’esercizio finanziario chiuso nel 2025 ed è stata multata per 2 milioni di euro. Avendo inoltre registrato un rapporto costo rosa superiore al 70% per l’anno solare 2025, al club giallorosso è stata inflitta un’ulteriore sanzione da 4 milioni di euro. Infine, Milan, Monaco, Besiktas, Inter, Paris Saint-Germain, Royal Antwerp e Trabzonspor hanno rispettato l’obiettivo finale del settlement agreement, conformandosi alla football earnings rule nella stagione 2025/26, relativa ai periodi di rendicontazione chiusi nel 2023, 2024 e 2025. Per questo motivo, i club sono usciti dal regime di settlement. La Prima Camera continuerà a monitorare i club ancora sottoposti ad accordo transattivo nel corso della stagione 2026/27 #UEFA #Football #Settlement

There is an expected earnings boom in markets right now. But if you look under the hood a lot of it seems to be coming from unrealised gains in stakes of companies that are due for IPO. 📈📉 https://t.co/ogiClS4gNN #EarningsBoom #IPO #MarketTrends #Nospecificcountriesarementionedinthetweet.

🇺🇸 #SPX | Highest Number of S&P 500 Earnings Calls Citing “#Oil” Since 2020 - Factset https://t.co/nM6uDGpk0e https://t.co/Gp644cDwSk #SPX #Oil #EarningsCalls #US

Es gibt eine simple Wall-Street-Formel: Wie viel mehr werfen Aktien ab als "sichere" Staatsanleihen. Diese Zahl liegt im Mai 2026 praktisch bei Null. Das letzte Mal so niedrig war sie kurz nach dem Platzen der Dotcom-Blase. Die Formel heißt Equity Risk Premium und ist einer der ältesten Bewertungs-Maßstäbe der Wall Street. Sie misst, wie viel zusätzliche Rendite Anleger für das höhere Risiko von Aktien gegenüber einer US-Staatsanleihe bekommen. Aktuell beträgt dieser Aufschlag noch rund 0,2 Prozentpunkte. Der S&P 500 wirft auf Basis der erwarteten Gewinne der nächsten zwölf Monate eine Rendite von etwa 4,78 Prozent ab. Eine zehnjährige US-Staatsanleihe lag am Freitag bei 4,57 Prozent. Wer heute einen US-Aktien-ETF kauft, bekommt rechnerisch fast genau das, was eine garantiert zurückgezahlte Staatsanleihe abwirft. Diese Zahl erscheint mitten im Aufwärtstrend. Der S&P 500 hat acht Wochen in Folge zugelegt, die längste Gewinnserie seit Ende 2023. Auch der Dow Jones notiert auf Rekordniveau. Im Hintergrund dieser Rekorde schrumpft der Bewertungs-Vorteil von Aktien gegenüber Anleihen auf Null. Eine zweite, unabhängige Bewertungsmethode kommt zum gleichen Ergebnis. Sie heißt Shiller-KGV und wurde vom Nobelpreis-Ökonomen Robert Shiller entwickelt. Sie zeigt, wie viel Anleger heute für jeden Dollar Gewinn zahlen, den die S&P-500-Konzerne im Schnitt der letzten zehn Jahre tatsächlich erwirtschaftet haben. Aktuell zahlt der Markt 42 Dollar für jeden Dollar Gewinn. Im Schnitt der letzten 140 Jahre waren es nur 17. So hoch wie heute war der Markt erst ein einziges Mal: im Dezember 1999, kurz vor dem Platzen der Dotcom-Blase, bei einem Wert von 44. Shiller hat aus dieser Bewertung eine zusätzliche Kennzahl abgeleitet, die direkt misst, wie viel Mehrrendite Aktien gegenüber sicheren Staatsanleihen versprechen. Über die letzten 140 Jahre lag dieser Aufschlag im Schnitt bei rund 3,3 Prozent pro Jahr. Heute beträgt er 1,33 Prozent. Auch nach dieser zweiten Rechnung werden Aktienanleger für ihr Risiko ungewöhnlich schlecht entlohnt. Die Aktien-Bewertungen liegen seit Jahren hoch. Die entscheidende Bewegung der letzten Monate kommt aus dem Anleihemarkt. Vor dem US-Israel-Angriff auf Iran Ende Februar lag die zehnjährige US-Treasury bei 3,96 Prozent. Heute steht sie bei rund 4,5 Prozent, ein Anstieg um etwa 0,6 Prozentpunkte in drei Monaten. Der Brent-Ölpreis liegt deutlich über dem Jahresstart und notiert bei rund 95 Dollar. Die US-Erzeugerpreise sind zuletzt im schnellsten Tempo seit 2022 gestiegen. Die einst sichere Annahme von Zinssenkungen in 2026 ist weitgehend ausgepreist. Trader rechnen inzwischen mit einer Wahrscheinlichkeit von 40 Prozent für eine Fed-Erhöhung im Dezember. Don Calcagni, Anlagechef von Mercer Advisors, beschreibt die Lage im Wall Street Journal nüchtern. Zwischen dem Anleihemarkt und dem Aktienmarkt habe sich eine Diskonnektion aufgebaut. Der eine signalisiere wachsende Inflations-Sorgen, der andere ignoriere die hohen Bewertungen. Um die aktuellen Kurse zu rechtfertigen, müssten die US-Konzerne mehrere Jahre lang außergewöhnliches Gewinnwachstum liefern. Calcagni halte das für unwahrscheinlich. Die Bullen halten ein gewichtiges Gegenargument bereit. Die KI-Investitions-Welle stehe erst am Anfang. Die großen US-Cloud-Konzerne planen für 2026 Investitionen von rund 670 Milliarden Dollar in Rechenzentrums-Kapazität. Die erwartete Gewinn-Wachstumsrate für den S&P 500 liegt bei 21 Prozent für 2026, 14 Prozent für 2027 und 11 Prozent für 2028. Wenn diese Zahlen halten, verschiebt sich die Mathematik von allein. Höhere Gewinne senken das KGV bei stabilen Kursen, der Earnings Yield steigt, und der Risiko-Aufschlag gegenüber Anleihen weitet sich wieder aus. Die Mathematik lässt nur zwei Wege aus dieser Lage. Entweder die KI-Gewinne kommen wie versprochen und drücken das KGV von oben, oder die Kurse passen sich der Bewertung an und drücken es von unten. Eine dritte Option ist in den Zahlen nicht enthalten. Wenn dich solche Makro Insights interessieren und dir helfen, interagiere gerne mit dem Post. 🧡 #Aktienmärkte #Investitionen #Wirtschaft

⚠ Wednesday Brief ⚠ 🇺🇸 Focus on #Nvidia Earnings 🇨🇳🌏 Xi Calls for Urgent End to Middle East War 🇬🇧 U.K. CPI Surprised Downward 🇪🇺 🇨🇳 Eurozone Trade Deficit with China Kept Rising ... https://t.co/0DutSc1kYa #Nvidia #MiddleEast #CPI #US #CN #GB #EU

🇺🇸 #Nvidia shares set for $350 billion price swing after earnings, options show - Reuters https://t.co/8SFksqUalw #Nvidia #Earnings #StockMarket #US

🌎 Asset allocators increased equity exposure by the most on record, moving to a net 50% overweight from 13% last month — the highest overweight in stocks since January 2022 - Bloomberg *BofA strategists led by Michael Hartnett attribute the move to a surge in earnings optimism #EquityMarkets #Investing #EarningsOptimism #Nospecificcountriesarementionedinthetweet.

Investors are becoming increasingly concerned that U.S. stock markets, despite strong earnings and optimism surrounding artificial intelligence, have not fully accounted for the risks of rising inflation and spiking bond yields, which could significantly impact valuations and economic growth amidst ongoing geopolitical uncertainties. #StockMarket #Inflation #Investing #US #IR

Investors are expressing concern that the current high U.S. stock market valuations do not account for rising inflation risks and increasing bond yields, which could impact economic growth and corporate profits, despite a recent surge in earnings driven by artificial intelligence and other positive factors. #StockMarket #Inflation #Investing #US #IR

Investors are cautioning that the U.S. stock market, currently buoyed by strong earnings and AI optimism, has not adequately accounted for the risks of rising inflation and bond yields, which could lead to a significant market correction amid geopolitical tensions and high energy prices. #StockMarket #Inflation #InvestmentRisks #US #IR

Investors are increasingly concerned that U.S. stock markets, buoyed by strong earnings and AI optimism, have not adequately accounted for the risks posed by rising inflation and escalating bond yields, especially amid ongoing geopolitical tensions in the Persian Gulf that could profoundly affect market dynamics. #StockMarket #Inflation #InvestmentRisks #US #IR

Investors are increasingly concerned that the buoyant U.S. stock markets, driven by strong earnings and AI optimism, have not yet accounted for the risks of high inflation and rising bond yields, which could lead to significant market corrections if geopolitical tensions persist and borrowing costs increase. #StockMarket #InflationRisks #EconomicOutlook #US #IR